Article courtesy of Fidelity

See options on how to handle this major expense in retirement.

Key takeaways

- Health care continues to be one of the largest expenses in retirement.

- Decisions about when to stop working, when to take Social Security, and how to generate cash flow in retirement all factor into how you prepare to meet health care expenses.

- To help fill a gap in saving for health care expenses, consider increasing contributions to your tax-advantaged accounts, especially HSAs (if you have one), which enable tax-free spending on health care in retirement.1

If you are like most Americans, health care is expected to be one of your largest expenses in retirement, after housing and transportation costs. But unlike your parents’ generation, you won’t likely have access to employer- or union-sponsored retiree health benefits. So health care costs will likely consume a larger portion of your retirement budget—and you need to plan for that.

There are a number of drivers behind this mounting retirement health care cost challenge. In general, people are living longer, health care inflation continues to outpace the rate of general inflation, and the average retirement age is 62 for most Americans—that’s 3 years before you are eligible to enroll in Medicare.

“Health care is creating a ‘retirement cost gap’ for many pre-retirees,” says Steve Feinschreiber, senior vice president of the Financial Solutions Group at Fidelity. “Many people assume Medicare will cover all your health care costs in retirement, but it doesn’t. So you should carefully weigh all options.”

How much is needed for health care costs in retirement?

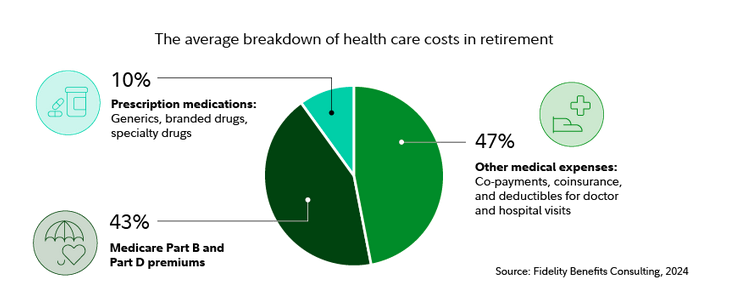

On average, according to the 2024 Fidelity Retiree Health Care Cost Estimate, a 65-year-old individual may need $165,000 in after-tax savings to cover health care expenses.

This amount is up nearly 5% from 2023.

Of course, the amount you’ll need will depend on when and where you retire, how healthy you are, and how long you live. The amount you need will also depend on which accounts you use to pay for health care—e.g., 401(k), HSA, IRA, or taxable accounts; your tax rates in retirement (see chart); and potentially even your gross income.2

Tip: If you’re still working and your employer offers an HSA-eligible health plan, consider enrolling and contributing to a health savings account (HSA). An HSA can help you save tax-efficiently for health care costs in retirement. You can save pretax dollars (and possibly collect employer contributions), which have the potential to grow and be withdrawn tax-free for federal and state tax purposes if used for qualified medical expenses.3

Pre- and early retirees: Make the most of your time to prepare

As retirement nears, you will have several big decisions to make, including when to stop working, when to take Social Security, how to pay for health care, and how to generate cash flow from your retirement assets. These decisions are interconnected and could make a difference in your living costs and lifestyle in retirement—and when you can retire.

Approximately one-third of “early retirees” who claim Social Security at age 624 do so to help pay for health care expenses until they are eligible for Medicare coverage at age 65. But if you can postpone retirement or save enough to cover health care costs until 65, then you may be able to defer your Social Security benefits. Generally speaking, the longer you can wait (until age 70) to take Social Security benefits, the more you can collect, assuming you live a long life.

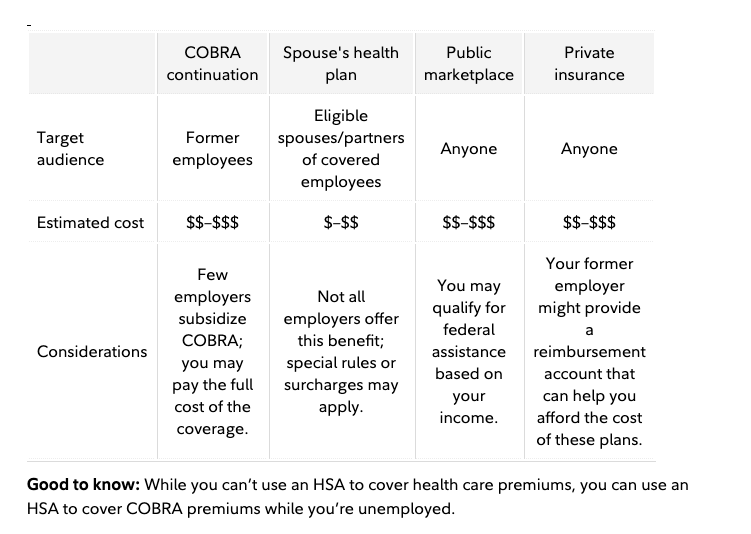

If you’re like most people, you probably don’t have access to employer-sponsored pre-65 retiree medical coverage. So if you retire prior to age 65, you’ll need to find coverage until you are eligible for Medicare. Consider these options that may be available to you (see table).

Turning 65 and retiring: Consider Medicare and other options

When you get close to age 65, spend some time reviewing and considering all your Medicare options. When you do become eligible at age 65, you’ll want to remember to sign up during your 7-month initial enrollment period that begins 3 months before the month you turn 65.

There’s a lot to learn about the world of Medicare. You’ll need to know about Medicare Parts A, B, and D, as well as Medicare Advantage and “Medigap” supplemental insurance plans.

In brief:

- Part A covers hospital costs after you meet a deductible.

- Part B is optional coverage for medical expenses and requires an annual premium. If you didn’t get Part B when you were first eligible, your monthly premium may go up 10% for each 12-month period you could’ve had Part B but didn’t sign up. In most cases, you’ll have to pay a penalty each time you pay your premiums, for as long as you have Part B. Moreover, the penalty increases the longer you go without Part B coverage.

- Part D is for prescription drug coverage.

- Medicare Advantage plans are all-in-one managed care plans that provide the services covered under Part A and Part B of Medicare and may also cover other services that are not covered under Parts A and B, including Part D prescription drug coverage.

- Supplemental policies, referred to as Medigap policies, are offered by private insurance companies to supplement expenses that Medicare Parts A and B do not typically cover.

Tip: You may be better off paying a higher premium but not having to pay out-of-pocket at your office visits. Look at the cost of annual premiums and co-pays at different levels of supplemental insurance. Compare these costs. Then factor in the number of visits and co-pay/co-insurance per visit that you anticipate for the next year.

Once you select a Medicare plan, it’s not forever. You can switch Medicare plans as you age and as your situation changes. (This does not apply to Medigap policies, however.) Generally, it makes sense to enroll in Medicare Parts A, B, and D when you are first eligible because the late enrollment penalties for doing so later are steep (see next section if you are continuing to work after age 65). For example, you may owe a late enrollment penalty if you go without Part D or other creditable prescription drug coverage for any period of 63 consecutive days after your initial enrollment period.

Turning 65 and still gainfully employed (or your spouse/partner is)

If you’re still working when you’re 65 and get health insurance through your employer or your spouse’s employer, you’ll have the opportunity to enroll in Medicare when you leave your employer plan through a Special Enrollment Period.

In addition to Medicare options to consider, if your spouse or partner continues to work, they may be able to cover you through their health plan. Talk to your HR department to help you evaluate all your options, costs, and any restrictions. The rules of Medicare are complicated, so to get started, consider the following questions:

- Which option provides the best coverage for your health needs, Medicare or the plan offered by your (or potentially your spouse’s) employer?

- Your employer is required to offer you coverage, but is that your best option?

- Is it more expensive to stay in your employer plan or join Medicare?

- Can your spouse or partner remain in your employer’s plan if you decide to leave?

Tip: Remember, one of the key goals at this stage is to avoid any gap in coverage.

Health care in retirement: Costs can come later

As you plan for health care expenses throughout your retirement—however long it may be—understand how paying for future health care expenses fits into your overall retirement income planning efforts, because health care utilization tends to increase as we age.

“Although health care costs continue to rise, there are financial planning steps that you can take today to help prevent health care costs from eating into your retirement lifestyle,” Feinschreiber advises. “For example, if you’re age 50 or older, you may be able to make up for a savings shortfall with additional catch-up contributions to your 401(k) or IRA. In addition, if you are age 55 or older, you can make an additional $1,000 catch-up contribution annually to your health savings account.”

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Contact

Phone

(505) 269-0817

Location

6565 Americas Pkwy NE, Suite 200 Albuquerque, NM 87110