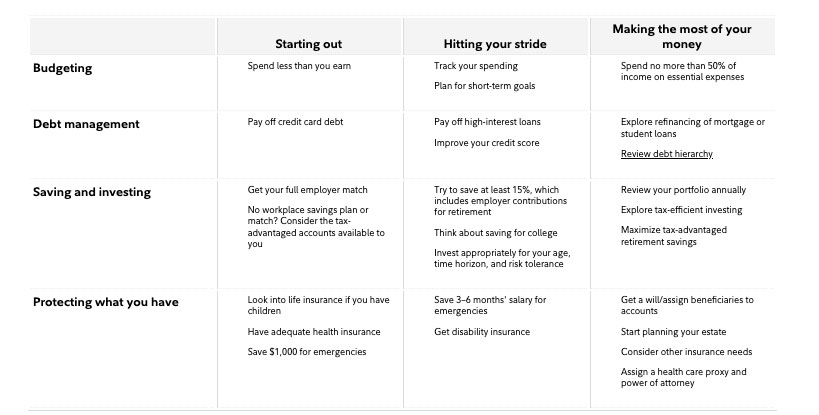

Setting small goals on your way to the larger ones can help with your long-term motivation and gradually strengthen your finances. For example, we suggest saving 3–6 months’ worth of essential expenses in an emergency fund. That’s a lot of money and can take a while. But saving $1,000 for emergencies while you continue to build your savings and live your life is easier to accomplish.

Making sure each of your 4 tiers is as strong as possible is the ultimate goal. The tiers are all interconnected—if one piece of your financial foundation is unsteady, it may not take much to throw off your entire plan. The areas you start with will depend on your unique situation; including where you’re starting from and where you want to go in the future.

Implement: Make your plan a reality

Knowing what needs to be done is half the battle. But you may also need specific strategies to help put your plan into action.

For instance, not everyone is a born saver—it can be a challenge to manage day-to-day spending or pay off debt. Mastering your budget could free up more money to save for the future and help pay down credit cards and loans. If you’re able to, increasing the amount you save by as little as 1% can have a huge impact over time.

A strong foundation of budgeting, debt management, saving, and insurance can help you achieve big, long-term savings goals, like retirement or funding a child’s education. But investing is a key component in a long-term plan as well. Investing in a mix of stocks, bonds, and short-term investments can help your money grow and potentially get you to your goals faster than saving alone.

But it does take time—that’s why getting invested as soon as possible is often one of the first steps in a financial plan. An investment mix tailored to your goals and time frame, your financial needs, and your feelings about investment risk can help find the balance between risk and reward that’s right for you.

Investing is important for long-term growth, but you have to be able to stick with it through the market’s ups and downs. Having a plan that’s built for the long haul and customized to your needs and preferences can help you do it.

Monitor and manage

The financial planning process never really ends—it should be ongoing. After putting your plan into action, it may be useful to check in at regular intervals to gauge how much progress has been made. You should be able to find out where you stand now relative to your goals and see what else needs to be done. As your life changes, your plan can change too. Any big developments like getting married or divorced, having a baby or adopting, or a change to your employment could require updates to your plan.

Investment monitoring and rebalancing are important components of this step as well. After all, markets change and may result in you taking on more risk than you are comfortable with—or not enough. A good rule is to review your asset mix and investments at least annually, and make adjustments as needed.

Plan for the future and live in the moment

Organizing your full financial picture may take time but it’s worth it. Before you begin, it can seem overwhelming. Taking action and working through the process one step at a time can help you feel in control and confident that you’re making the most of your money.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Contact

Phone

(505) 269-0817

Location

6565 Americas Pkwy NE, Suite 200 Albuquerque, NM 87110